{kind=link}

The rise of direct bookings over OTAs

Hotel distribution trends in EMEA and APAC

from 2017 to 2020

Following our very widely circulated study on the distribution landscape of Europe, up to 2018, we wanted to update the study and include the Asia-Pacific* region to compare and see if the trends are global or regional.

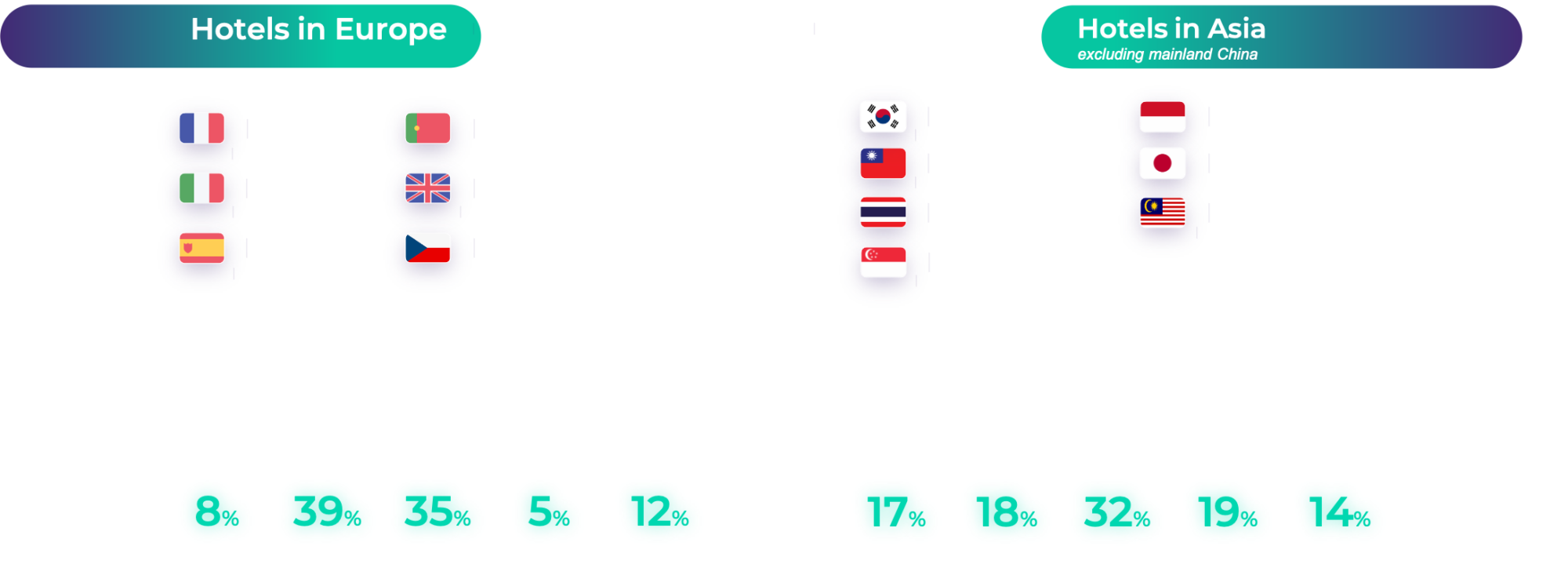

We have gathered information from over 3,400 hotels in Europe and 450 hotels in the Asia-Pacific region* to understand how the hotel distribution landscape is evolving. The study focuses on the last three complete years (2017 to 2019) and considering the sea change that our industry has suffered – it includes 2020 broken into three sections (see methodology section for more details).

Key findings

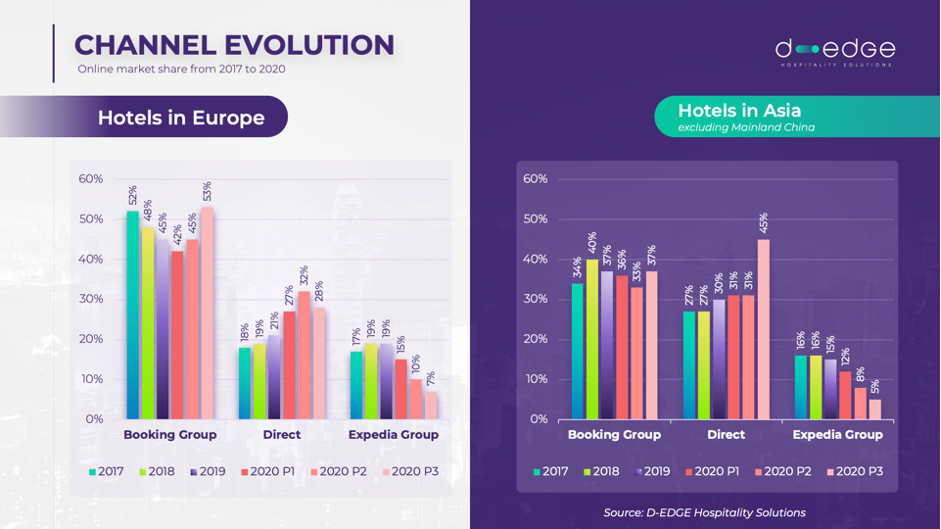

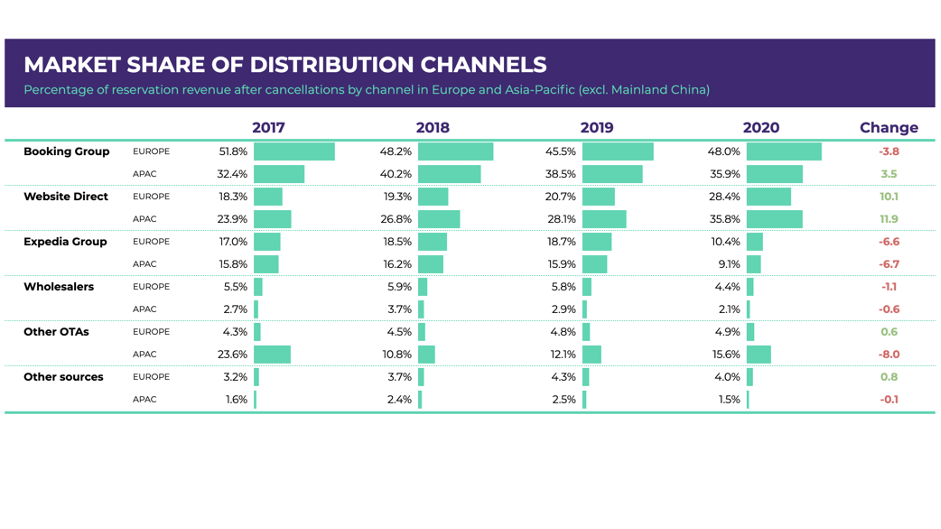

1- The share of Website direct revenue has seen consistent growth in both Europe and Asia-Pacific since 2017 and has accelerated in 2020 gaining a total of 10 percentage points.

2- OTAs have lost, on average, 10 percentage points of market share in Europe and Asia-Pacific from 2017 to 2020.

3- The loss in OTA market share is due to Booking.com group losing market share between 2017 and 2019, and in 2020 with Expedia losing a 60% market share loss- to the benefit of direct bookings and Booking.com group.

4- The close similarities between Europe and Asia-Pacific indicate that these trends are not isolated to European hotels or a small segment but indicate global hotel distribution tendencies.

Additional Findings

- Since the lockdowns, Booking.com Group has grown to over 53% market share in Europe.

- During the June to September 2020 period, the Asia-Pacific* area has shifted to 45% direct distribution making it the most important channel in the region.

- In general, Asia-Pacific* hotels have a more balanced distribution mix than Europe.

- Due to the pandemic, cancellation rates in 2020 have grown by 10 points on average compared to 2019.

- Website direct remains the channel with the lowest cancellation rate.

Methodology

For this study, we picked a consistent sample of D-EDGE hotel customers from 2017 to 2020 that had a consistent spread of distribution channels over the selected period.

For 2020, we broke the year down into three phases:

- Phase 1 covers January and February before the pandemic started

- Phase 2 runs from March to May, which corresponds to the first wave of global lockdown

- Finally, Phase 3 runs from June to September, the phase of uncertain reopenings and cautious recovery.

Distribution channel trends got upended in 2020

Although it is not statistically possible to compare market share changes from previous years to 2020, when reviewing the two periods together, and comparing the Asia Pacific* and Europe regions, indicates interesting trends that arise from the 2020 pandemic and how the findings relate to past averages.

In Phase 3 of 2020, Europe saw a surge in market share by Booking.com group – mostly at the expense of Expedia while Website Direct gained traction and became the leading channel in Asia*.

At D-EDGE we believe that it may be linked to the relaxed cancellation policies of Booking.com and their market position for “free Cancellations” that give them a strong position on the current market conditions. Regarding Expedia, one assumption is that their strength in Europe was very focused on bundling flights with hotels and negotiating deals. Post-lockdown, this has become a much harder sell.

Hotels in the Asia-Pacific* region have seen a similar evolution during 2020, with Website Direct becoming the primary source of online revenue, and Booking.com group remaining in a similar range. Similar to Europe, Expedia has lost the most in market share compared to previous levels.

It is important to note that as shown in the Methodology section, volumes of booking in 2020 are much lower and represent a very different demographic than previous averages. However, the average trends are of a strong interest in understanding how the recovery will play out.

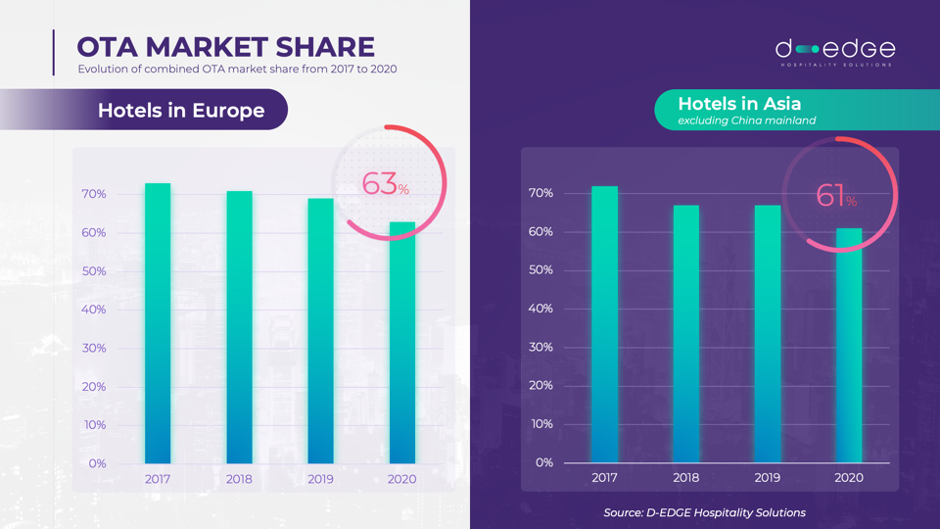

OTAs dominate but grow negatively

While OTAs are experiencing a loss in market share in both Europe and Asia-Pacific*, they remain, in both markets, the dominant source of online revenue. With 63% of market share in Europe and 61% in Asia-Pacific, the similarities in both regions show a trend that is likely global.

Both regions have seen online distribution growth over the last three years. In 2019 Asia-Pacific* region saw a 35% growth in online distribution (all online channels combined) compared to 2017 (across the same hotels and distribution channels). European growth over the same period was not as fast with 17% growth from 2017 to 2019.

Looking further into the various channels, it becomes evident that website direct has been taking market share from the OTAs. This trend accelerated in 2020, which is possibly explained by the reduction in advertising by OTAs while Website Direct kept a level of online advertising. When OTAs reduce their advertising budgets, organic results for hotels rank higher in search engines resulting in sales on hotels websites.

We have noticed an increase in customers desiring a direct relationship with hotels. Especially during times of uncertainty in restrictions and fast-changing regulations, guests prefer to be in direct contact with their hotels.

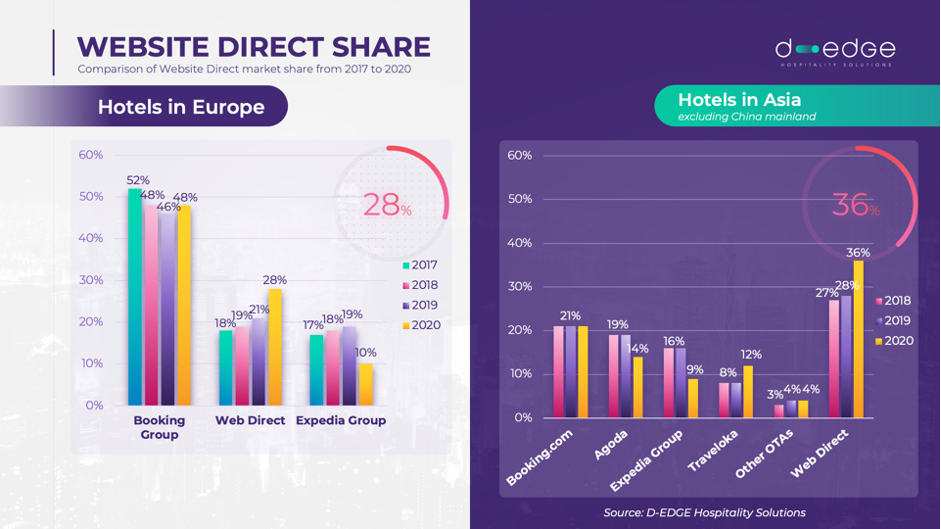

Website Direct: a rising second

Both Europe and Asia-Pacific have Website Direct revenue as the second-largest online revenue stream (in the Asia-Pacific region it is the largest if Booking.com group revenue is segmented) and has recorded a steady growth for several years. However, the Asia-Pacific area leads with 8 points more than Europe in 2020.

The significant growth during 2020 in Website Direct for this study can be explained in part to the fact that the study only counts D-EDGE customers for which we have continued to advertise despite the pandemic.

As also covered in our previous study of hotel advertising trends, increased advertising and optimisation of ad spendings on a larger number of channels contribute to the multiplication of revenue from Website Direct.

Website Direct revenue in Europe is quite evenly distributed across the hotel category. However, the high-end and luxury segments have a slightly higher share of Website Direct (four-star at 21% and five-star at 24%) compared to the mid-range and budget hotels (3-star at 19% and 2-star at 15%). In Asia-Pacific, the 3-star category dominates the Website Direct revenue, with 32% of their distribution.

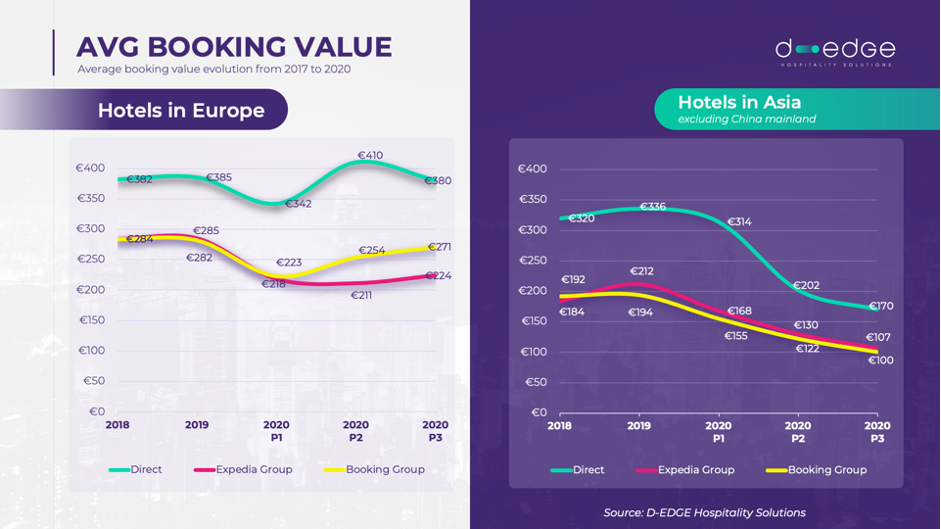

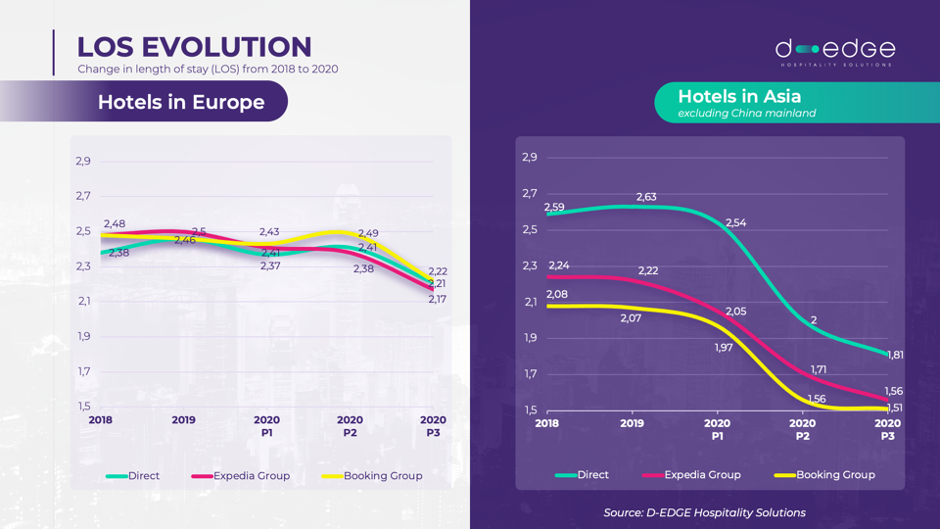

Booking behaviour evolution

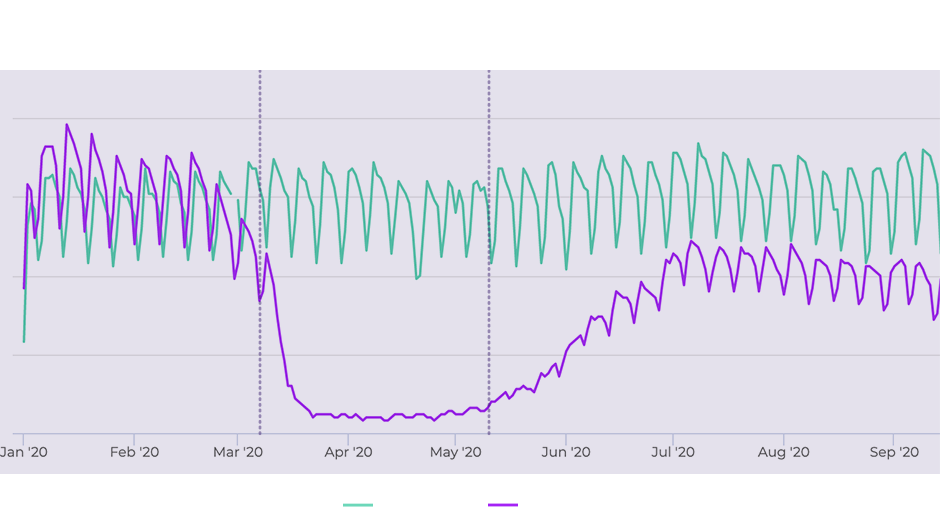

In addition to market share shifts, we looked into the booking behaviour from 2018 to 2020. For 2020 we separated the year into three phases, as explained in the Methodology section.

Hotels in Europe have a relatively stable rate and booking value, whereas Asia has seen the value drop quite substantially in 2020. This is attributed to a steep drop in the length of stay in the Asia-Pacific area, much steeper than in Europe, and probably a rate policy of lowering rates in an attempt to stimulate demand.

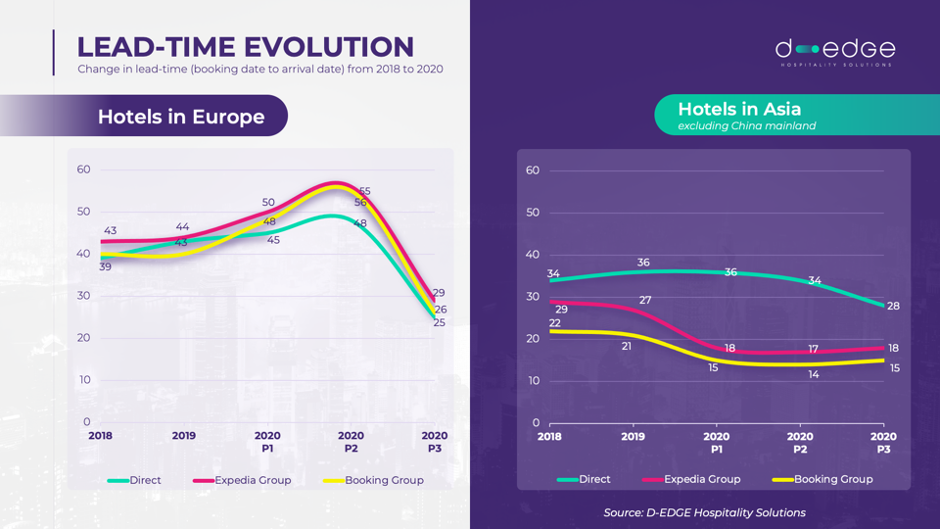

Lead time, on the other hand, saw a sizable shift in Europe. Moving from an average of 32 days in 2019, down to 27 in the post-lockdown phase. This pattern was observed across all booking channels. Asia-Pacific shows a very different curve and no sudden peak during the lockdown period.

Length of Stay has changed more dramatically in Asia-Pacific than in Europe. This is likely due to the nature of travel in 2020, which shifted away from tourism to necessary travel, hence the shorter time. We believe these trends are quite temporary and will change again when more certainty exists in travel.

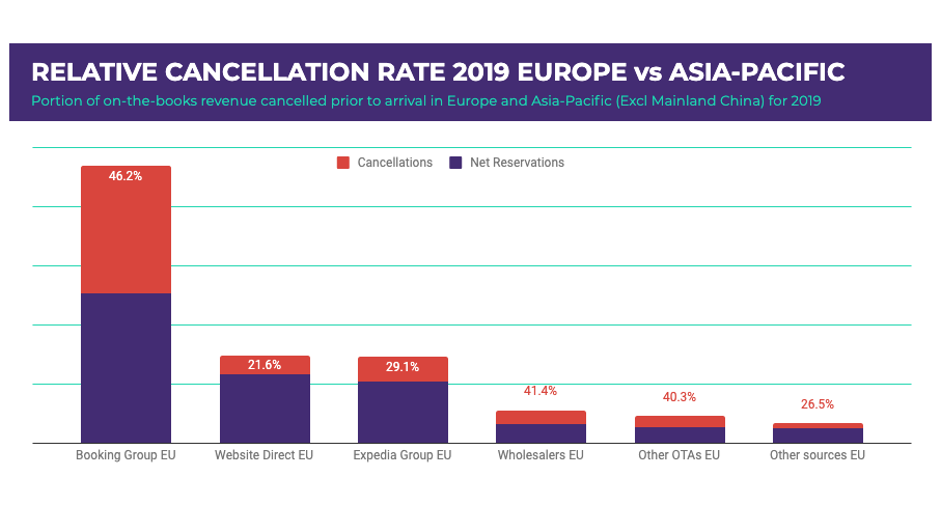

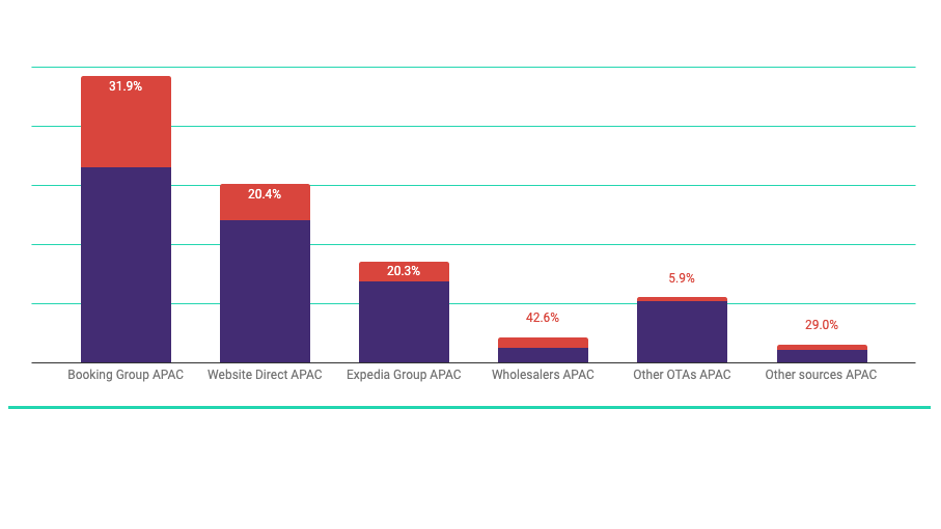

Cancellation rates: an endless issue

Growing cancellation rates have been plaguing hotels internationally; however, the Asia-Pacific area has a much lower cancellation rate than European hotels. Due to the pandemic, we are not comparing the cancellation rates for 2020. We’re analysing the cancellation rates for 2019.

In Europe, during 2019, 25% of reservations were cancelled before arrival and that 25% of reservations represented 38% of on-the-books revenue. However, in Asia-Pacific*, a much smaller percentage is observed: 14% of reservations were cancelled over the same time period. The 14% reservations represented 25% of on-the-books revenue.

We believe that part of the reason for the difference in cancellation rates is the travel distances in Asia-Pacific being much larger than Europe which makes travel booking and planning more important. It is also due to different cancellations practices by the OTAs in APAC. Agoda, for example had, until the COVID context, a very restrictive cancellation policy (thus a low cancellation rate), but now offers flexibility to adapt to current demand.

Distribution of cancellation rates is quite similar in both regions, with Booking.com group having the highest rate. In 2019, Booking.com Group made 100% more cancellations than Expedia or Direct in Asia-Pacific*. Despite that, it is worth noting that Booking.com group generates the most revenue for those markets. The gross reservations from the Booking.com group are so much higher than any other channel that it is intriguing to speculate how much market share they would own if their cancellation rate would be on par with the rest of the channels.

Conclusion

2020 has changed the hotel distribution market – not just the volumes which experienced record lows – but more significantly, the trends. Surprisingly, several of those shifts were already in motion before the pandemic. They were just accelerated.

OTAs losing market share in a market that has seen steady growth until 2020, shows that strategies hotels have been implementing to balance their distribution channel weights have been paying off. Even though we are entering a phase where distribution profitability will be less important than distribution volume, hotel distribution managers should remain conscious of how long it has taken them to successfully shift channels from being dominated by OTAs.

While similar in many ways, European and Asia-Pacific online distribution for hotels is evolving a little differently in the face of the 2020 pandemic. Easy cancellations have been the largest winning category in Europe while more direct relationships are becoming the biggest category in Asia-Pacific. The importance of having a strong direct channel is not to be under-estimated for the future of hotel bookings, as travellers seek clear communications and reassurance for their bookings.

Working out the balance between direct and reassuring channels, where guests know they can communicate with and manage their bookings without surprises while maintaining a fair cancellation policy and re-booking for guests, will be essential to retain as much business as possible in the foreseeable future.

Due to the current uncertain conditions around booking travel and hotels, it is more important than ever to have reassuring communications with the guests before they book and to understand their needs, preferences, and habits. We recommend hotels to invest in CRM technology and ensure they have a connected technology stack to ensure bookings, emails, past emails etc. are managed smartly.

*excluding Mainland China

You may also like

How is hotel distribution evolving in Europe and Asia?

Data, trends and strategies to optimise your hotel’s performance…

D-EDGE, a global leader in hospitality technology, today announced the appointment of Frédéric Kingue Johnson as its new Chief…

Peak season is almost here, now is the time to refine your operations to ensure a seamless guest experience and hit your…