{kind=link}

Hotel distribution and the pandemic: the travel chessboard

How hotel distribution evolved in EMEA and APAC from 2018 to 2021

In the past 15 months, the hotel industry has suffered one of the most significant losses in gross booking quantity ever. However, despite volumes in 2020 being 69% lower than the previous year, we have been monitoring the reservation types, channels and rates to gain insights into trends that could help hotels plan the recovery.

In 2019 we published our first analysis of distribution trends, titled A Deep-dive into European Hotel Distribution trends 2014-2018, in which we uncovered the sheer volume of cancellation rates from OTAs and how this was affecting hotels. The report laid out a lot more on how the industry, at its peak during the study, was changing.

Our second analysis in 2020 was broadened to look into the trends not only in EMEA but also in Asia-Pacific (APAC). The report, called The Rise of Direct Bookings Over OTAs, brought to light how patterns had changed due to the pandemic, and how direct bookings were taking a much bigger part of a much smaller market.

This study is the follow-up to our 2020 partial analysis. In this report, we examined the year 2020 in its entirety (to better understand the impact of the pandemic), and reviewed the first five months of 2021. The information included in this research has been gathered from 3,442 hotels in Europe and 438 hotels in the Asia-Pacific region.

Key findings

- The Website Direct channel surpassed Booking and OTAs in Asia* (41% share), and is the second largest in Europe (32%)

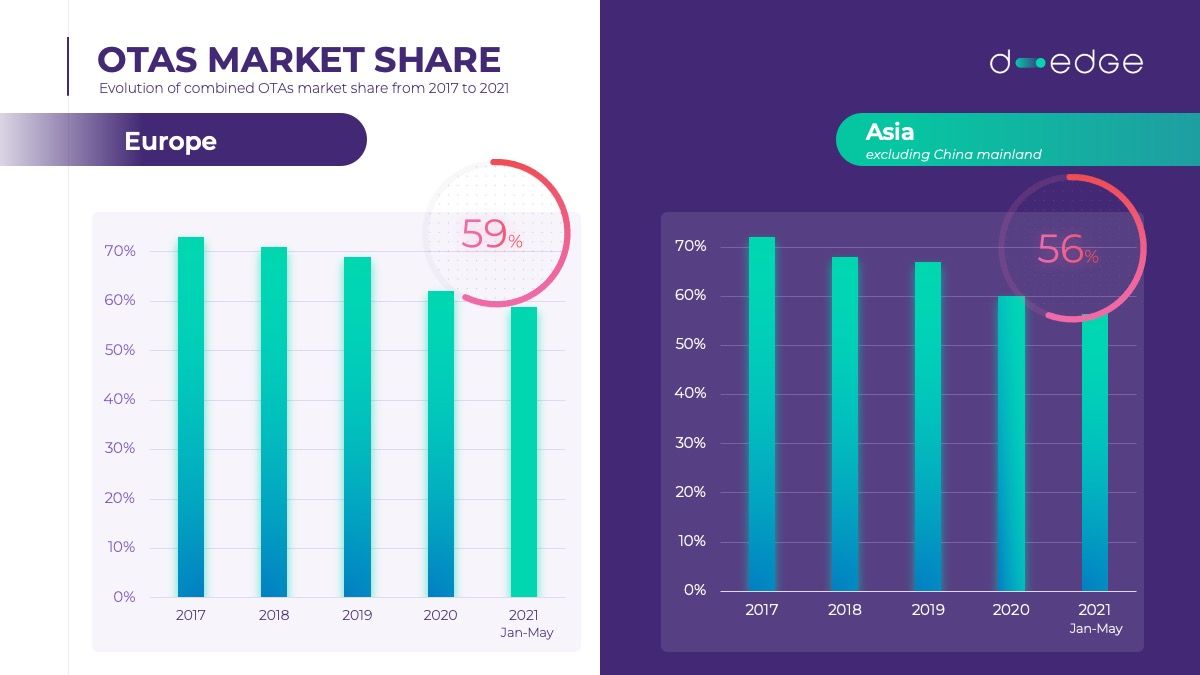

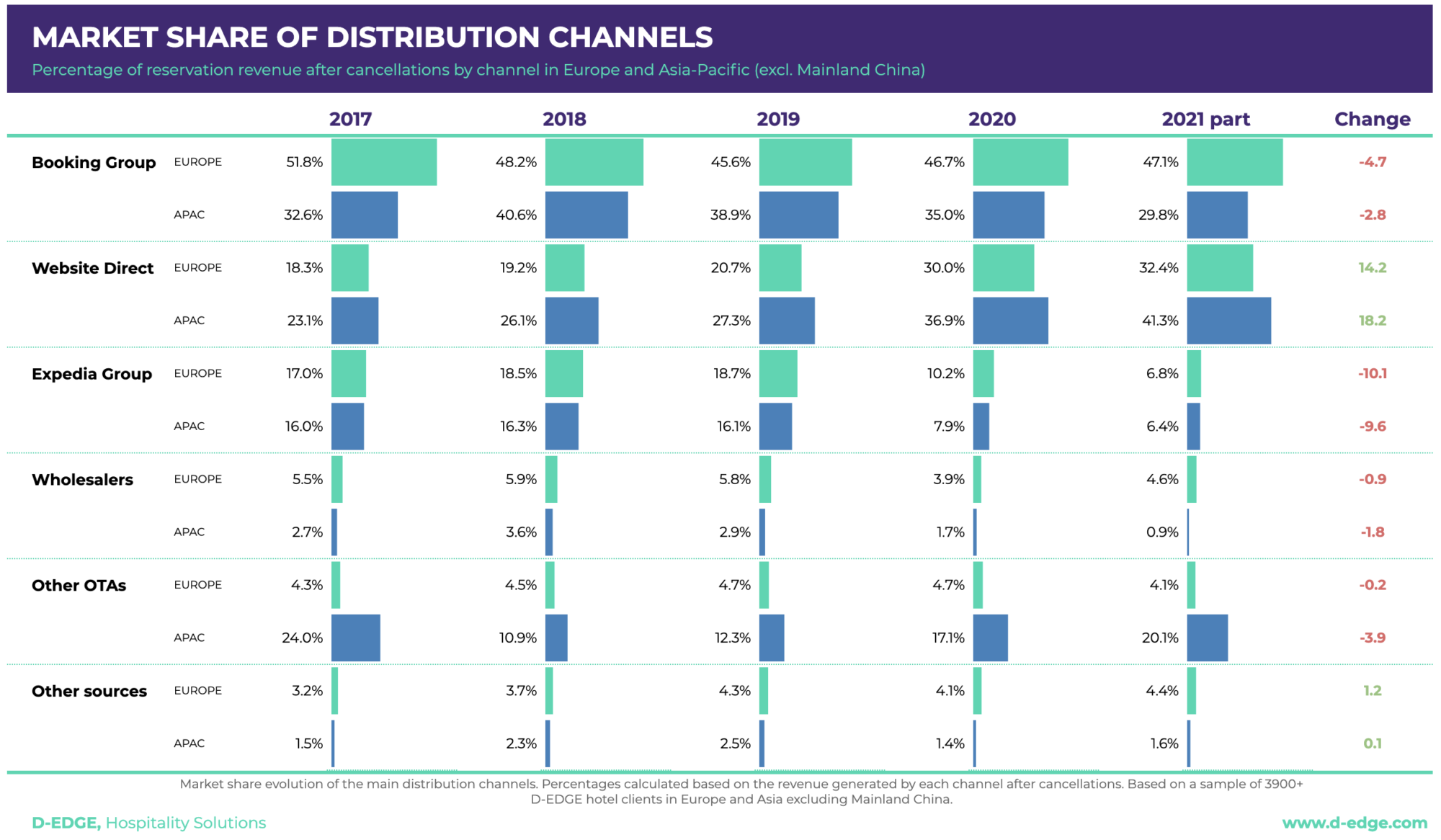

- In 5 years, OTAs’ market share has declined by 11 points in Europe and by 14 points in Asia*

- Expedia’s loss of market share continues, losing 12 points in Europe and 10 points in Asia-Pacific*

- European average Hotel Booking Value increases by 12% in 2021 showing renewed confidence and demand for travel

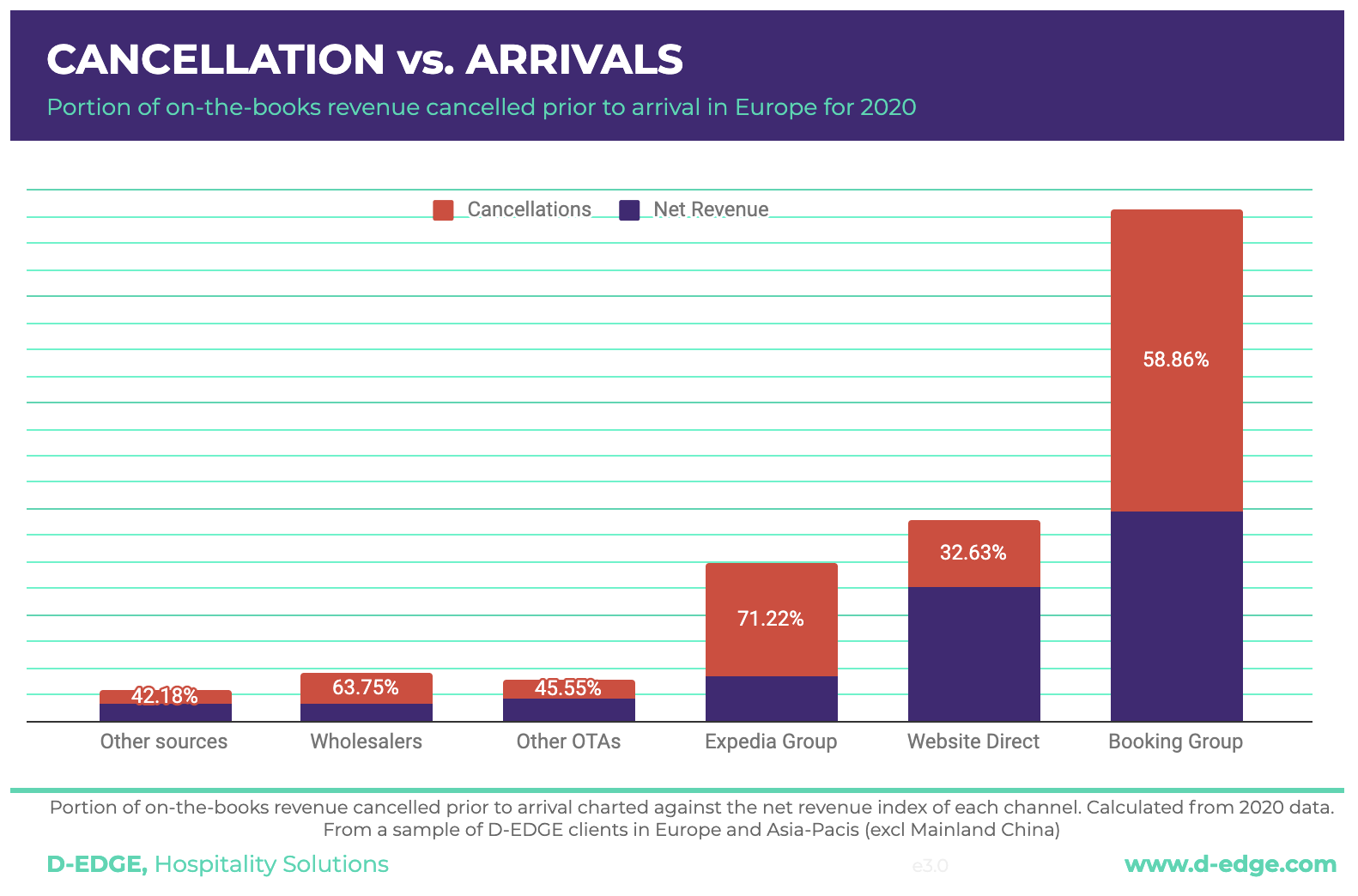

- In 2020, Cancellation doubled with Expedia hitting 71% cancellations and Booking almost 60%. In Eruope, we expect to return to 2019 levels as demand picks up and travel rules stabilise.

Global booking trends: recovery is still fragile

Globally speaking, the reservation volume in 2021** is still 40% lower than 2019 figures — but 159% above the March to May months of 2020. That being said, the EMEA market shows promising signs of improvement, while APAC, after an initial recovery, saw a steady decline, mainly due to the new lockdowns.

The recovery is happening and we can see that once restrictions are lifted there is evidence of pent-up demand in the markets. However, the recovery is fragile with high levels of uncertainty which is affecting prediction beyond one or a maximum of two months ahead. This is affecting cancellation rates as we discuss below.

Direct booking growing faster and faster

In the 2020 report on hotel distribution we had observed that Website Direct bookings were one of the fastest-growing channels, however take into account that gross reservation volumes are much lower. We cover some of the reasons for increased Website Direct in section IV below.

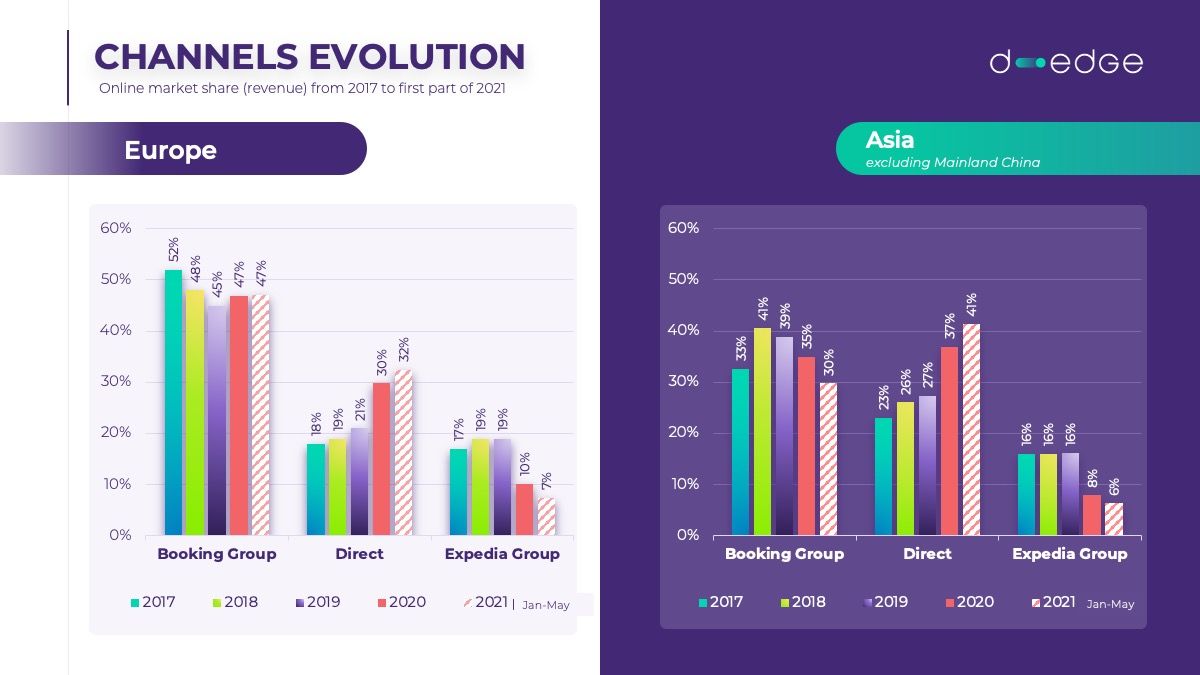

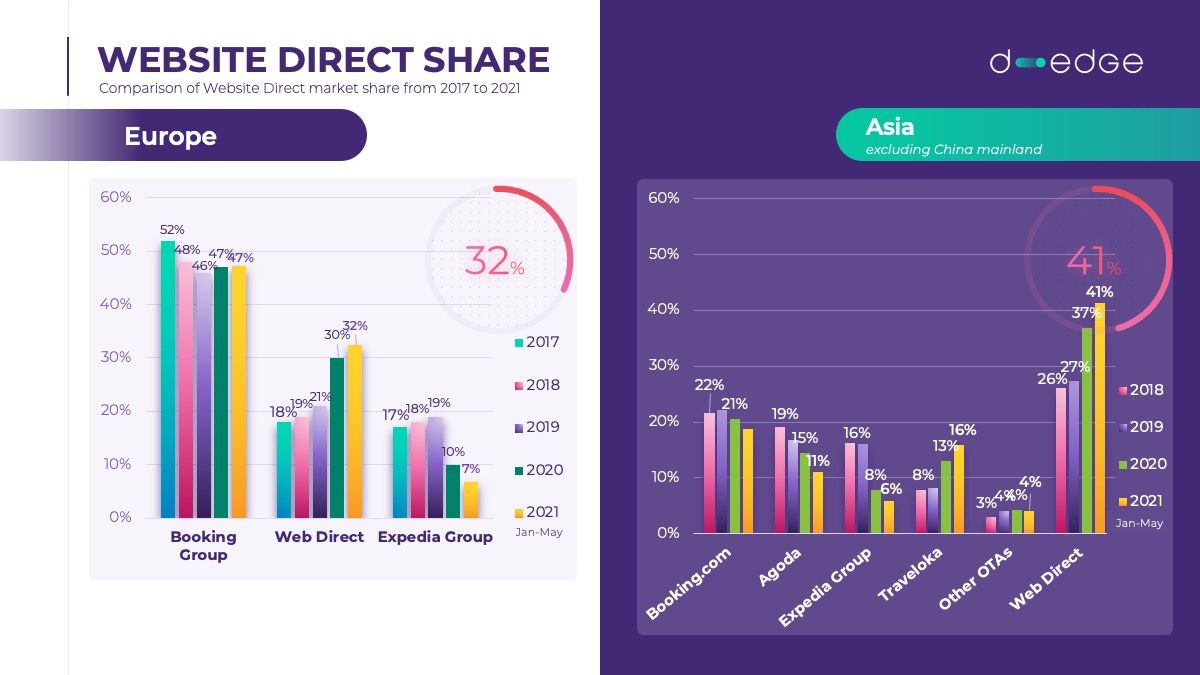

In 2021, we saw a continued increase in revenue generated by the direct channel. In Europe, almost one third of the total reservations are produced by Website Direct and, in APAC*, direct became the leading channel, both in 2020 (37%) and in 2021** (41%). This surge was mainly at the expense of Expedia, which showed equivalent negative numbers in both regions: 7% market share in 2021** for Europe versus 10% in 2020 and 6% in 2021** versus 8% in 2020 in APAC*.

Pushing the analysis to June 2021, we even observe that for this later month, in Europe, Website Direct is the first and, so far, the only channel in which booking levels are back, to the pre-pandemic levels.

Website direct surpasses Booking.com in APAC*

In Asia*, direct became the main source of revenue already in 2019, and it increased its market share even more solidly in 2020, reaching the all-time best result of 41% in 2021**. We believe the higher number of local travellers since the beginning of the pandemic may explain this peak of direct reservations in the last 15 months, as proximity tourists made the majority of traveling in ’20-’21, and they are, usually, less likely to book via an OTA, preferring direct channels.

OTAs are losing market share

In our previous hotel distribution study, we had already pointed out how OTAs were experiencing a loss in market share in both Europe and Asia-Pacific. Even though they remain, in both markets, the dominant source of online revenue, this negative trend persisted in 2021. Especially in Asia*, OTAs’ market share decreased by four points, going from 60% in 2020 to 56% in 2021**. If we look at the last five years, OTAs market share in Asia* dropped by 14 points (from 70% to 56%). Continuing the trends we had observed in 2020, the pattern is even more visible in the first few months of 2021**. Last year, we speculated that this drop might have been caused by the reduction in advertising by OTAs, resulting in higher rankings in search engines for website direct. Most Online Travel Agencies resumed some SEA actions in 2021, even though not at the same levels of 2019, so the causes should be searched somewhere else. At D-EDGE, we believe this may be due to a combination of reasons:

- More relevant information on hotel websites when compared to OTAs, especially regarding anti-COVID measures,

- More flexible policies on website direct,

- Rate disparity favoring direct channels, especially on metasearch engines,

- More domestic/local travellers, with no need for air transportation,

- The lower overall volume of bookings giving preference to frequent travellers who are more informed about the advantages of booking direct.

However, this negative dynamic is not applicable to all OTAs, and some players stood out:

- Booking.com, the undisputed leader, has shown a strong resilience, especially in Europe, accounting for 47% of the hotel bookings revenue generated in the region.

- Airbnb, even though they have a much smaller market share (in hotel distribution), grew steadily over the last five years. And, with a market share growth of 20x, it’s worth keeping an eye on. If interested in this channel, we recommend you watch the webinar we held with Airbnb “How to get started on Airbnb”.

- Some Local OTAs have benefited from a strong growth likely due to increased domestic demand and have shown to be a good source of additional bookings for hotels. For example, in Hungary Szalla.hu has gone from 7% to 12% of the hotels online sales between 2019 and 2021**. In the Czech Republic, Hotel.cz has grown its market share by more than 300%. In the Netherlands, Hotelspecials.nl has multiplied its share by 26x. And in Indonesia, Traveloka has grown from 53% to 58% of the market share and Ticket.com has grown from 7.65% to 14%.

More than ever, having a smart mix of distribution channels is of great importance.

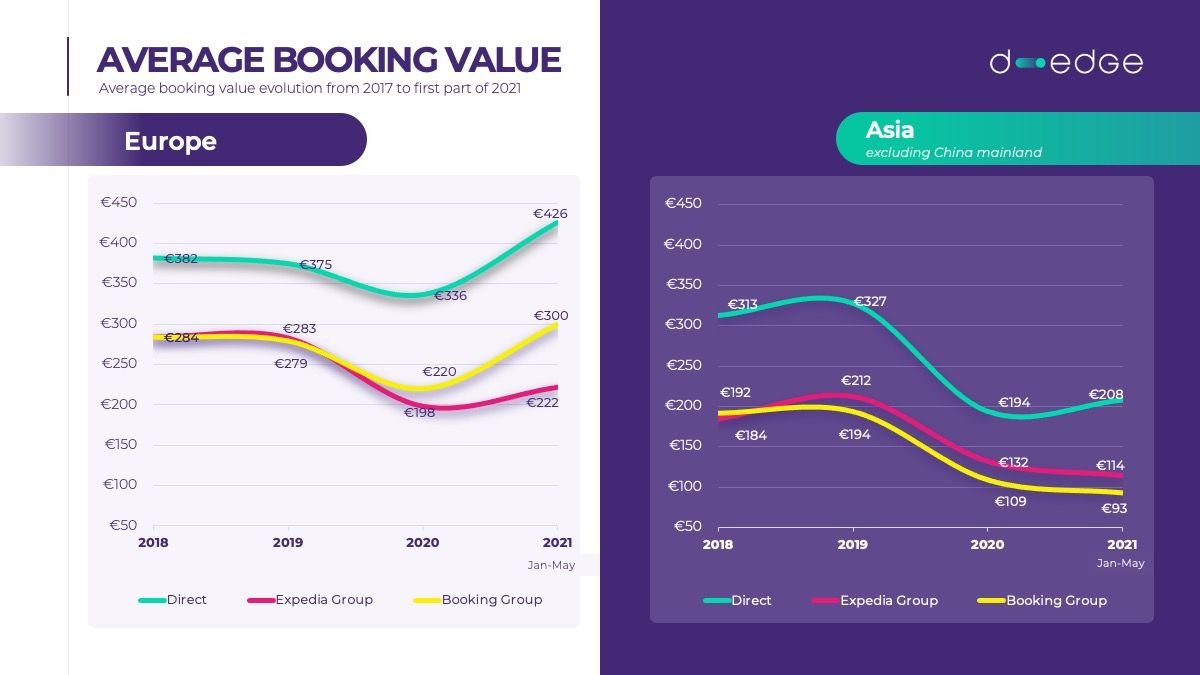

Booking Value is back in Europe

Average booking value decreased dramatically in 2020, for both Europe and Asia*. However, in Europe, over the first part of 2021** it came back to 2018 levels (with the exception of reservations coming from Expedia) for European properties. It’s worth mentioning that average booking value in Europe surpassed both 2018 and 2019 levels, contributing to the higher value of bookings. APAC* shows different numbers, with a drop of booking value that is steady, except for website direct, even though it is still far from pre-pandemic figures. In this region, Booking Group’s booking value is around half of what it used to be in 2018. Again, this may be explained by the majority of travel being local in ’20-’21, and consequently, to a shrinking length of stay that is addressed in the next section.

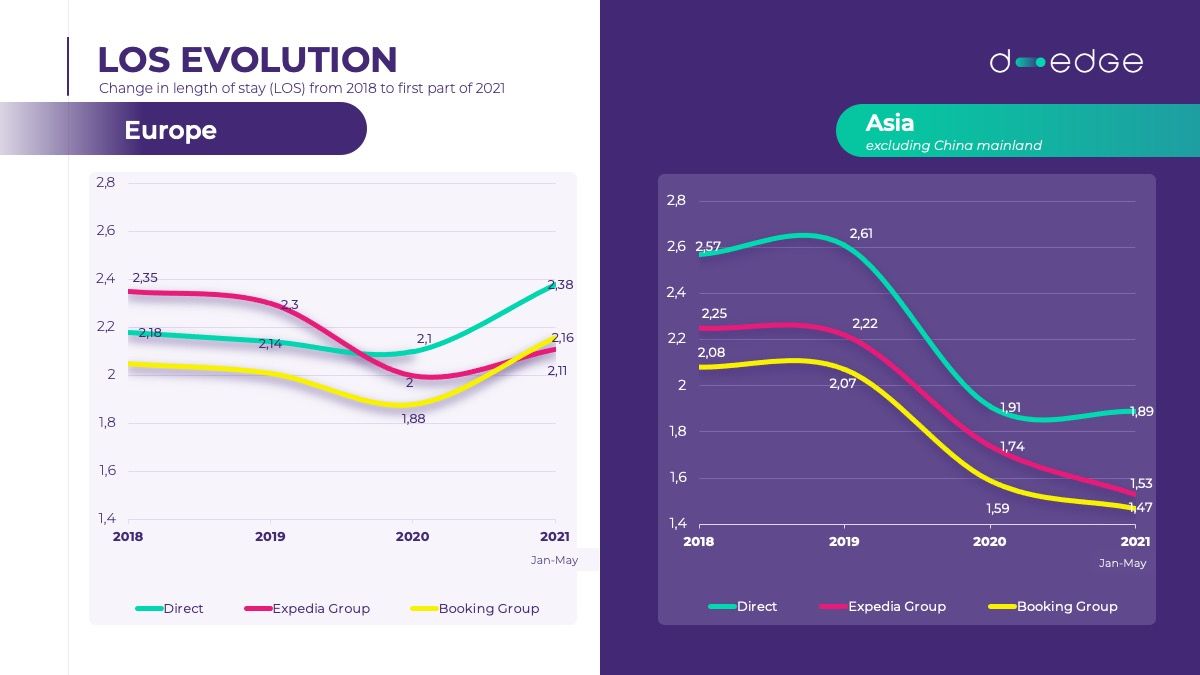

Length of stay is down in APAC*

The average length of stay decreased dramatically in Asia while returning to pre-pandemic levels in Europe. This is probably because most of APAC travel in ’20 and ’21 was domestic, in a region that usually has a higher length of stay and is more accustomed to longer travel time than Europe. Because of the fast-changing travel restrictions inside the region, the risk for cancellation remains, unfortunately, very high.

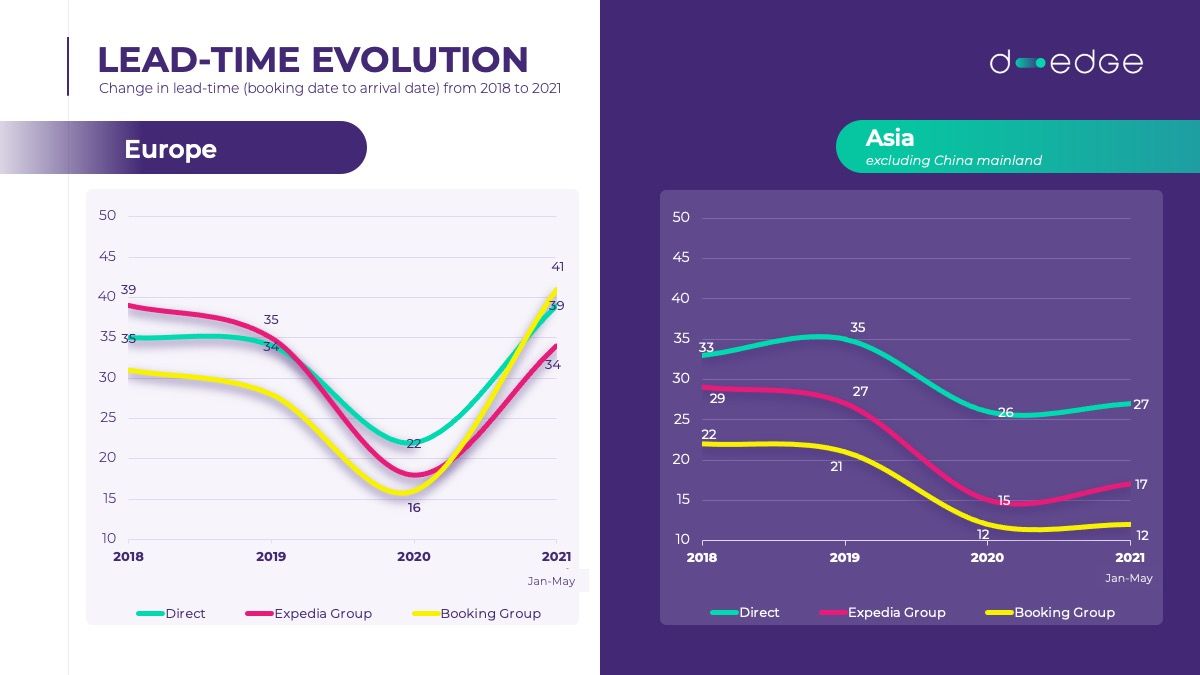

Lead-time is better than pre-pandemic levels in Europe

Even when it comes to lead-time, Europe and Asia show very different numbers. While the booking window in Europe reached – and in some cases, even surpassed – pre-pandemic figures, this is not the case for APAC*, where the lead-time remained virtually identical to last year, probably due to the fact that travel restrictions remain very heavy in this region. With the reopening of almost all countries in Europe, in the spring of 2021, travellers have regained confidence with a vital need to prepare for their holidays in advance. Hence this very strong increase in lead time in Europe.

However, as we cover in the next section, these lead times need to be seen through the lens of Cancellations which are, understandably, at an all-time high with the fast-changing travel restrictions and lockdowns.

The year of cancellations

During the pandemic, we witnessed the decline of not refundable rates in hotels. The vast majority of reservations made in 2020 and 2021** are, in fact, flexible. This is not surprising, due to the instability created by the pandemic: new variants of the virus, ever-changing restrictions on travel, etc.

With virtually 100% of reservations being refundable, it’s not unexpected that the cancellation rate rose as well. In 2021**, particularly, almost six out of ten bookings have been canceled on Booking Group. The situation is even more alarming for Expedia, surpassing the 71% cancellation rate. Direct channel, again, shows better results, with “only” 1/3 of reservations being canceled before arrival.

Compared to our first Hotel Distribution Analysis these cancellation rates have more than doubled for almost every channel except Website Direct, which has remained the channel with the lowest rate of cancellations.

While the years prior to the pandemic had seen a gradual improvement in cancellation rates we believe that high cancellations will be standard in the foreseeable future. We recommend hotels adapt and learn to work with cancellations, for example by communicating with guests as much as possible in advance of any changes, sharing information related to their stay, re-confirming their booking, or encouraging an early cancellation for dates where demand is rising. Using a connected CRM tool where such communications can be automated and friendly will help hotels avoid last-minute cancellations for days where hotels would otherwise be full.

Conclusions

While we are seeing some stability in bookings in EMEA we advise hotels to remain agile and guest-first in their approach to revenue for the rest of 2021. The demand for travel exists and restrictions are being eased, which we are seeing in the demand. But as these restrictions are changing frequently, hotels should ensure they are keeping the guest informed and helping the guests when changes occur so they return as soon as they can.

The rise in Website Direct and the increased reliability (lower cancel rates) in those bookings have renewed the importance of the channel. Hotels should take advantage of this time to review their website and ensure it is up to the latest standards. Changes in tracking standards across the internet make it even more important to update one’s website now, fully integrated hotel websites are becoming mandatory to correctly measure the efficiency of marketing and improve the guest experience.

Look for more niche distribution channels where you can capture the domestic market or OTAs in countries where you believe there could be a potential market for you. Working with your Channel Management provider, grow the list of distribution channels you work with and maximise your chances of being seen.

As an industry, we can safely predict that there will be a lot of changes in the coming 12 months. We recommend hotels work with their solution providers and stay abreast of best practices since these will likely be completely different, quarter to quarter and even month to month.

* Excluding mainland China

** January to May 2021

You may also like

A guide to strengthening your direct distribution strategy

4 profiles, 4 ways to book. What this means for your hotel website and…

How is hotel distribution evolving in Europe and Asia?

Data, trends and strategies to optimise your hotel’s performance…

D-EDGE, a global leader in hospitality technology, today announced the appointment of Frédéric Kingue Johnson as its new Chief…